When a lender reviews your mortgage application, they are not simply asking whether you earn enough money. They are asking a more precise question: what percentage of your income goes toward housing, and what percentage goes toward all your debts combined? The answers live inside two ratios — GDS and TDS — and understanding them can mean the difference between an approval and a phone call telling you the file didn't work.

What GDS Actually Measures

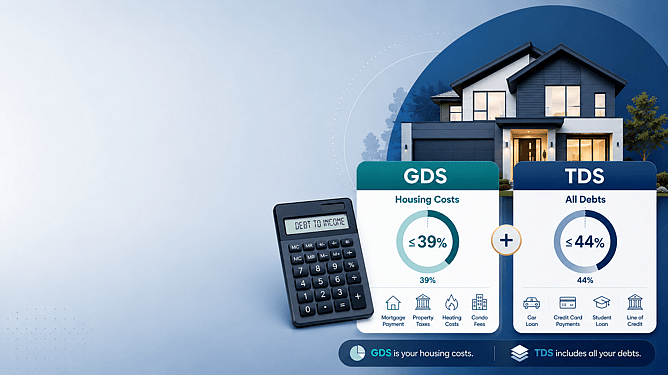

The Gross Debt Service ratio, or GDS, looks specifically at your housing costs. It takes the sum of your monthly mortgage payment (principal and interest), property taxes, heating costs, and, if applicable, half of any condo maintenance fees, then divides that total by your gross monthly income. The result is expressed as a percentage.

Most lenders want to see a GDS ratio at or below 39 percent for insured mortgages — those with less than 20 percent down — and some conventional lenders allow a little more flexibility. The underlying logic is straightforward: if you're spending more than roughly a third of what you earn before taxes just to keep a roof over your head, the math becomes uncomfortable very quickly once you factor in everything else life requires.

Notice what goes into the GDS calculation. Heating is included because it is considered a necessary housing expense, not a discretionary one. Condo fees appear at 50 percent rather than the full amount because the assumption is that a portion of those fees covers building maintenance rather than pure housing cost. Property taxes are included in full because they are unavoidable. The mortgage payment itself uses the qualifying rate, which under the federal stress test is higher than the rate you'd actually pay — more on that in a separate article.

What TDS Adds to the Picture

The Total Debt Service ratio takes everything in the GDS calculation and adds your other monthly debt obligations on top — car loans, student loans, credit card minimum payments, lines of credit, and any other fixed debt payments. That combined number is then divided by your gross monthly income.

The standard TDS threshold is 44 percent for insured mortgages. Again, some lenders will flex slightly in specific circumstances, but 44 percent is the benchmark that frames most approvals.

The gap between GDS and TDS tells the story of your overall financial obligations. A borrower with a GDS of 32 percent and a TDS of 43 percent is carrying significant non-housing debt — perhaps a car loan and a student line of credit — and is very close to the ceiling. A borrower with a GDS of 35 percent and a TDS of 36 percent has very little outside debt, which is a healthier profile even though their housing ratio is higher.

Why These Ratios Matter When You're Close to the Limit

Being near the threshold is not automatically disqualifying, but it changes the conversation. If your TDS is sitting at 43.5 percent, even a small increase in the purchase price can push you over. Lenders work with precise numbers, and a ratio that exceeds the guideline — even by a fraction — can mean the file needs to go to a different lender, requires a larger down payment, or needs some debt to be paid down before closing.

This is where working with a broker becomes genuinely useful. A broker can model your ratios across different scenarios — different purchase prices, different down payment amounts, paying off a specific debt before applying — and show you exactly where the levers are. The ratios are math, and math can be managed once you understand the inputs.

It is also worth knowing that different lenders use slightly different guidelines. The 39 percent GDS and 44 percent TDS thresholds are standard for insured mortgages regulated under the National Housing Act, but alternative and private lenders operate under different frameworks entirely. If a borrower doesn't fit within those thresholds at an A lender, there are paths forward — they just look different.

Making It Work for You

The most common mistake borrowers make is not knowing their ratios before they start house hunting. They find a home they love, make an offer, and then discover in the qualification process that the monthly payment combined with their car loan pushes TDS to 46 percent. At that point, options narrow and timelines compress.

Knowing your ratios in advance — or working with someone who can calculate them for you — means you go into the process with clear eyes. You know your real budget. You know whether paying off one debt before applying would meaningfully expand your options. You understand why the bank's number is lower than the mortgage calculator on their website suggested.

These two ratios are not bureaucratic obstacles. They are the clearest window into how lenders think about risk, and once you understand them, you can plan around them.

If you want to talk through how this applies to your situation, book a free clarity call at mortgagefernando.com/clarity-call.