While the world breathes a collective sigh of relief over the recent easing of geopolitical tensions in the Middle East, a secondary, quieter story is unfolding right here at home. For Ontario homeowners, buyers, and business owners, this global shift is triggering a chain reaction that directly impacts your wallet, your property value, and your next mortgage decision.

To understand where mortgage rates are heading this summer and fall, we have to look at how global capital markets are reacting to stability.

The Resource Boom Meets a Cooling Market

Canada is fundamentally a resource-heavy, commodity-driven economy. Over the past few months, the global economy has been searching for a secure, stable supply of oil, gas, and critical minerals. Canada has stepped up as a massive stabilization point. We are seeing a monumental 10-to-15-year energy outlook take shape, driven by British Columbia’s LNG progress and a renewed push for undersea LNG reserves off the coast of Nova Scotia—providing European markets with a safer, shorter supply route than the Middle East.

However, the immediate, short-term impact of global peace talks is a correction in energy prices. Crude oil has stabilized, dropping roughly $10 per barrel from the mid-90s down to the low-80s.

While lower oil prices mean slightly less immediate GDP heat for a resource exporter like Canada, it also means something far more important for everyday borrowers: inflation is losing its fuel.

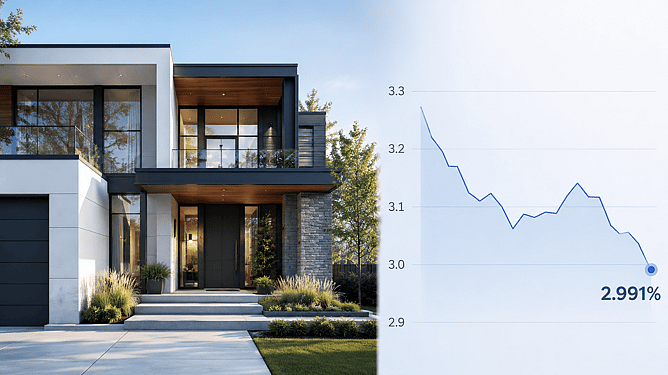

The Bond Market Has Already Reacted

Mortgage rates don't wait for banks to change their minds; they follow the bond market. The Government of Canada 5-year bond yield—which directly backstops and drives fixed mortgage rates—reacted instantly to the news of global stability.

Yields have tumbled from the 3.24%–3.34% range down to around 2.99% in recent days. That is a swift 20 to 30 basis point drop.

Historically, when bond yields sustain a drop like this, fixed mortgage rates follow. Currently, major lenders are posting 3-year and 5-year fixed rates in the mid-4% range (around 4.3% to 4.5%), with non-major lenders hovering in the low 4.20s. As this bond yield drop settles in over the next few months, we anticipate fixed rates will begin leaning down toward the high-3% and low-4% range—returning to where they were before global volatility spiked.

The Domestic Reality: Deflation Risks

This rate relief is arriving just in time. The broader Canadian economy is currently flatlining, sitting uncomfortably in technical recession territory.

With economic growth stalled and oil prices cooling, Canadian inflation could easily drift below the Bank of Canada's 2% target over the next few months. If we enter a deflationary environment, the central bank will have no choice but to keep its foot on the interest rate relief pedal to stimulate domestic economic activity.

What This Means for Your Real Estate Strategy

If you are navigating the Ontario housing market as a homeowner or buyer, this convergence of events creates a highly strategic window:

For Active Home Buyers: We have seen record levels of inventory over the spring, though some tired sellers have recently begun pulling their listings. However, as trade agreements like the USMCA find clarity and interest rates stabilize in the "3-point-something" range, sidelined buyers will look to re-enter. With home prices down roughly 30% from their pandemic peak, the upcoming summer and fall markets represent a structurally stable entry point before competition intensifies.

For Variable-Rate Holders: If you have ridden out the highs of the variable market, keep a close eye on fixed-rate benchmarks. Getting a fixed rate with a "3" in front of it on a 3-year or 5-year term has historically represented a safe, stable long-term equilibrium for Canadian mortgages. If you see it, it may be the ideal time to lock in.

For the 2026/2027 Renewal Wave: The largest wave of Canadian mortgage renewals in history is approaching. If fixed rates pull back into the high-3% range, the "renewal shock" so many feared will be significantly mitigated.

Get Clarity Before the Market Shifts

When the market indicates stability, it moves quickly. Navigating flat economic growth, shifting inventory, and tumbling bond yields requires strategy, not guesswork. Whether you need to consolidate high-interest debt, review an upcoming renewal offer, or map out a purchase pre-approval, looking at the math early is the best way to avoid costly mistakes.

If you want clarity before making your next mortgage decision, let's look at your options together.

Marlon

You can book a clarity call here: mortgagefernando.com/clarity-call