Why This Matters Right Now

Buying a home in Ontario is expensive. That is not new information.

What is newer is a federal rebate that could meaningfully reduce the cost of purchasing a newly built or substantially renovated home for eligible first-time buyers — and an Ontario provincial component that could make the total relief significantly larger.

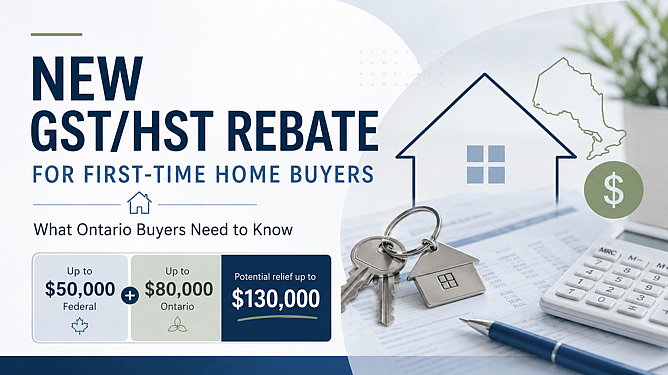

The federal First-Time Home Buyers' GST/HST Rebate can recover up to $50,000 in federal GST or HST for eligible buyers. Ontario has also announced proposed relief on the provincial portion of HST that could add up to $80,000 more. Combined, eligible Ontario buyers purchasing a qualifying new home could potentially see up to $130,000 in total HST relief.

That is a meaningful number. It deserves a clear-eyed look.

But this rebate is not for every first-time buyer, every property type, or every situation. Before a buyer builds their purchase plan around it, they need to understand what it actually covers, who qualifies, how they would receive it, and what can go wrong when the assumptions do not line up.

What Is the First-Time Home Buyers' GST/HST Rebate?

When you purchase a newly built home in Canada, GST or HST is generally applied to the purchase price. That tax can be substantial — particularly on higher-priced new construction in Ontario.

The First-Time Home Buyers' GST/HST Rebate is a federal program administered by the Canada Revenue Agency (CRA) that allows eligible first-time buyers to recover some or all of the GST or federal portion of HST paid on a qualifying new or substantially renovated home.

This is not a rebate for every first-time buyer. It is specifically aimed at buyers purchasing, building, or substantially renovating a new home to use as their primary residence. It is generally not applicable to ordinary resale homes, because resale transactions are typically exempt from GST/HST under standard rules.

How Much Could a Buyer Save Federally?

The federal rebate is structured based on the purchase price of the home.

Homes valued at $1 million or less may qualify for up to the full federal rebate — potentially recovering 100% of the GST or federal portion of HST paid, up to a maximum of $50,000, subject to actual tax paid and all eligibility conditions being met.

Homes valued between $1 million and $1.5 million may qualify for a partial federal rebate. CRA's own example indicates that a $1.25 million eligible new home may qualify for 50% of the maximum federal rebate — or approximately $25,000.

Homes valued at $1.5 million or more do not qualify for the First-Time Home Buyers' GST/HST Rebate under current federal rules.

In plain terms:

$900,000 new home: May qualify for the full federal rebate, subject to eligibility and actual GST/HST paid.

$1,000,000 new home: May qualify for up to $50,000 federally.

$1,250,000 new home: May qualify for approximately $25,000 federally based on CRA's published example.

$1,500,000 or more: No federal First-Time Home Buyers' GST/HST Rebate.

These figures assume all other eligibility conditions are met. The actual amount depends on the GST/HST paid on the transaction.

The Ontario Portion: Why the Number Could Be Much Larger

For Ontario buyers, the headline number could be significantly larger than the federal rebate alone.

Ontario has announced and proposed relief for the 8% provincial portion of HST on eligible new homes. That provincial component could be worth up to $80,000.

Ontario's budget materials indicate an intention to remove the full 13% HST for eligible buyers of new homes valued up to $1 million, with the maximum combined rebate of $130,000 maintained for new homes up to $1.5 million.

When you add the federal and provincial portions together, the total potential relief for an eligible Ontario buyer purchasing a qualifying new home could reach up to $130,000.

That is a meaningful reduction in purchase cost — but buyers need to be careful about how they treat this number.

The federal rebate is already being administered by CRA. The Ontario provincial portion has been announced and proposed, but buyers should confirm the final implementation details and verify how and when the Ontario amount will be received before incorporating it into a live purchase plan. The opportunity is real, but the assumptions need to be checked.

Who May Qualify?

Not every first-time buyer qualifies. CRA applies a specific definition.

To be eligible, a buyer generally must:

Be at least 18 years old

Be a Canadian citizen or permanent resident

Not have lived in a home owned by them, their spouse, or common-law partner as a primary place of residence in the current calendar year or in the previous four calendar years

Not have previously received the First-Time Home Buyers' GST/HST Rebate

Be purchasing, building, or substantially renovating a qualifying home to use as their primary place of residence

Meet the applicable timing conditions — the agreement of purchase and sale must generally be entered into on or after March 20, 2025 and before 2031

Construction or substantial renovation must generally begin before 2031 and be substantially completed before 2036

Ownership must generally transfer before 2036

If any of these conditions are not met, the rebate may not apply.

What Types of Homes Are Covered?

The rebate is generally for newly built or substantially renovated homes — not ordinary resale properties.

Eligible home types may include:

New-build houses and townhomes

New condominiums

Owner-built homes

Substantially renovated homes

Certain eligible co-operative housing situations

Most resale homes are not covered because GST/HST generally applies differently to new construction than to existing resale properties. If a buyer is comparing a resale purchase to a new build, this distinction matters in how the total cost of each option is evaluated.

What If You Are Buying a Newly Built Rental Property?

This is a common point of confusion that deserves a direct answer.

The First-Time Home Buyers' GST/HST Rebate is not designed for newly built rental or investment property purchases. It is focused on eligible first-time buyers buying, building, or substantially renovating a first home to use as their primary place of residence.

If you are purchasing a newly built property as a rental or investment, the more relevant program is generally the GST/HST New Residential Rental Property Rebate. The eligibility rules, forms, lease requirements, documentation, and timing for that program are different.

Ontario has also proposed enhanced HST relief related to new rental housing, but investors should verify the current details carefully before relying on it in their numbers.

Investors should confirm the applicable rebate, eligibility conditions, and process with their accountant, real estate lawyer, builder, and CRA before assuming any rebate applies to a rental purchase. Do not assume that because a rebate exists for new construction, it automatically applies to every type of new construction purchase.

How Would Buyers Actually Receive the Rebate?

This is where many buyers are surprised. The rebate does not always show up the same way, and assuming it will automatically reduce your closing costs can create a planning problem.

Option 1 — Builder credits the rebate at closing

In many new construction transactions, the builder agrees to credit the federal rebate to the buyer at closing. The buyer effectively receives the benefit as a reduction in the amount owing. The builder then files the rebate application with CRA directly. In this case, the buyer may not need to file a separate application for the federal portion, but they should confirm this clearly in the purchase agreement.

Option 2 — Buyer applies directly to CRA

If the builder does not credit the rebate at closing, the buyer may need to pay the full applicable amount and then apply to CRA directly for the rebate. CRA allows buyers to apply online through their CRA account or by mailing the applicable forms — Form GST190 is generally used for homes purchased from a builder. There is generally a two-year time limit from the date ownership was transferred to submit the application.

The Ontario portion

Ontario has indicated an intention to provide up to $80,000 of provincial HST relief and to align the Ontario rebate's effective period with the federal policy direction. However, the exact process for claiming or receiving the Ontario portion should be confirmed once the implementation details are fully finalized. Do not assume the Ontario amount will automatically appear at closing in the same way the federal portion might.

Before closing, buyers should ask: Is the builder crediting the federal rebate upfront? Has the builder already factored the rebate into the advertised price? Will the buyer need to apply directly? Has the Ontario portion been confirmed for this specific transaction?

Why Timing and Paperwork Matter

Being a first-time buyer is necessary — but it is not sufficient on its own.

The agreement of purchase and sale date, construction start and completion timelines, ownership transfer timing, occupancy, builder documentation, and application deadlines all matter. A buyer could be a legitimate first-time buyer in every sense and still not qualify for the rebate if the property, construction timeline, or paperwork does not align with the program rules.

Buyers should keep records of everything: agreements of purchase and sale, invoices, calculations, occupancy documentation, and rebate-related forms. CRA can delay or deny rebate claims when documentation is incomplete, calculations are incorrect, or required forms have not been submitted properly.

Rebate eligibility is a checklist, not just a status.

Mortgage Planning Implications

This is the most important section for any buyer who is actively planning a purchase.

A rebate that could be worth $50,000 federally — and potentially much more with the Ontario component — can meaningfully affect your cash position and purchase strategy. But it needs to be treated carefully.

Here is what buyers and their advisors should think through:

Does the rebate reduce cash required at closing, or is it received later? If the buyer must apply directly to CRA after closing, the rebate is not available on closing day. That affects how much cash the buyer needs on hand.

Has the builder already priced the rebate in? Some builders advertise prices that already assume the rebate reduces the effective cost. Buyers who count the rebate again are double-counting.

Does the buyer qualify for the mortgage without depending on the rebate? If the purchase only works financially because of an assumed rebate, and the rebate is delayed, reduced, or denied, the buyer is in a difficult position.

What if the rebate is delayed or handled differently than expected? Builder credit timelines, CRA processing times, and Ontario implementation mechanics can all affect when a buyer actually receives the benefit. A purchase plan that depends on the rebate being available immediately carries risk.

Are all other costs still accounted for? Land transfer tax, legal fees, adjustments, closing cost reserves, and other purchase-related expenses are still real regardless of the rebate.

Has the real estate lawyer reviewed how the rebate appears on the statement of adjustments? Buyers should not close on a new build without understanding exactly how the rebate is being applied and whether the representation in the purchase agreement matches what appears at closing.

The clearest way to think about it: a strong purchase plan should work before the rebate. The rebate should improve the plan, not hold the whole plan together.

My Takeaway as an Advisor

The First-Time Home Buyers' GST/HST Rebate — particularly with the potential Ontario provincial component — can make a genuine difference for an eligible buyer purchasing a qualifying new home in Ontario.

But the value of the rebate depends on the buyer meeting all the eligibility conditions, the property meeting all the qualifying criteria, the timing and paperwork aligning correctly, and the application process working as expected.

The rebate can improve a strong purchase plan. It should not be the foundation of a weak one.

If you are considering a new build, pre-construction purchase, or substantial renovation, it is worth reviewing the full picture before you sign or rely on the rebate. A mortgage planning conversation can help you understand your eligibility assumptions, the cash required at closing, how the rebate affects your financing structure, and whether the purchase still makes sense if the rebate is delayed, reduced, or handled differently than expected.

A Note on This Article

This article is for general information purposes only and should not be treated as tax, legal, or accounting advice. Rebate eligibility, application requirements, and available amounts should be confirmed with CRA, your accountant, your real estate lawyer, and your builder where applicable. The Ontario provincial component referenced in this article reflects announced and proposed provincial budget measures. Buyers should verify current implementation details before relying on the Ontario portion in a live purchase plan.