The Big Mystery of Mortgage Rates

You’ve likely seen mortgage ads that promise “as low as 3.99%!” But then you talk to a lender and somehow... your rate’s 4.69%.

What gives?

In Canada, mortgage rates aren’t one-size-fits-all. In fact, they vary wildly depending on one thing: how risky you are to a lender.

Just like car insurance companies charge more if you’ve had a few fender benders, mortgage lenders adjust your rate based on how likely they think you are to default. The lower the risk you pose, the lower the rate they’re willing to offer.

And that explains why your neighbour, cousin, or co-worker may have locked in a better rate — even if your situations seem the same on paper.

Let’s unpack this.

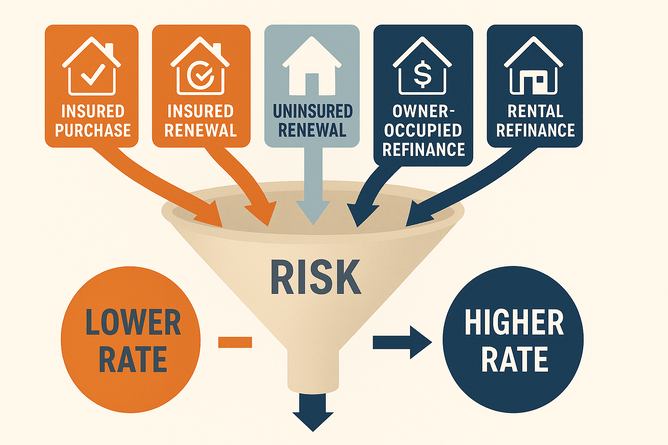

The Different Mortgage Buckets (And Why the Rates Change)

Canadian mortgage lenders break things down into categories — each with a different level of risk. Here are the main buckets:

1. Insured Purchases – The Cream of the Crop

When you buy a home with less than 20% down, you’re required to get default insurance from one of the “Big Three”: CMHC, Sagen, or Canada Guaranty.

Good news for the lender: they’re not on the hook if you default. The insurer pays out.

Because of this security blanket, lenders offer their best rates to insured purchases. Yes, you pay a premium for the insurance, but the trade-off is a lower interest rate.

Think of this like wearing a helmet and padding to the bank. You’re protected, and they appreciate that.

2. Insured Renewals – Keeping the Coverage

If your mortgage was originally insured and you haven’t refinanced, it stays insured when you renew. That means the bank still has a safety net.

And because you're not switching lenders (so they avoid sales commission costs), your current lender can offer a competitive rate.

But try moving to a new lender? Suddenly, sales costs pop up — and with them, a potentially higher rate.

3. Uninsured Renewals – Flying Without the Net

If your mortgage wasn’t insured — either from the beginning or because you refinanced — then you’re in the uninsured bucket.

Now the lender carries all the risk. If things go south, there's no backup.

That means slightly higher rates, even if your credit and income are strong. Again, your current lender might give you a better deal since they don’t have sales costs when you stay put.

4. Owner-Occupied Refinances – The Gray Zone

You’ve built some equity and want to refinance — maybe to consolidate debt or renovate. Seems straightforward, right?

Not to the lender.

Now they’re assessing you all over again: income, credit score, debt ratios, even whether your job is stable.

And because refinances can’t be default-insured in most cases, you’re now a riskier file. Rates are higher than on insured purchases or renewals.

You’re basically saying, “I want more money, and I’m not bringing insurance to the table.” The bank’s response? “Okay... but that’s gonna cost ya.”

5. Rental Refinances – The Riskiest of Them All

Ah yes, the rental property — the goldmine that could also become a money pit.

When you refinance a rental, lenders see layers of risk: tenant instability, vacancies, non-owner occupancy, market fluctuations, and more.

Even if you’ve got perfect credit, you’re asking for money on a property that you don’t even live in. Naturally, lenders charge a rate premium.

It’s the “you better be sure you can handle this” interest rate.

Why Lenders Get So Spooked: The Risk Matrix

Let’s spell it out: every borrower is not created equal.

Lenders assess your application through a filter of risk. The more boxes you check, the more “safe” you appear:

✅ Strong credit

✅ Stable, verifiable income

✅ Low debt-to-income ratio

✅ Owner-occupied home

✅ Property in a strong market

✅ Loan insured

Remove any of those, and the rate creeps up.

Here’s an example:

Jane, a salaried nurse, 5% down payment, buying a house in Ottawa for 650K = low risk, insured = lowest rate

Steve, self-employed contractor, 25% down on a rental in Sudbury for 650K = higher risk, uninsured = higher rate

Same mortgage amount. Totally different rates.

“But That’s Not Fair!” – A Common Frustration

Many people assume that they should get a rate because they saw it or were told about it.

But those rates are usually “teaser” rates — designed for insured purchases with excellent borrower profiles.

When the bank runs your numbers and sees you're self-employed, or you’re refinancing, or the property is a condo above a nightclub (true story), they adjust accordingly.

It’s not personal. It’s risk-based pricing.

How a Mortgage Pro Helps Lower Your Risk Profile

Here’s the good news: you can influence how a lender sees you.

And that’s where a seasoned mortgage professional (like me!) becomes your secret weapon.

We don’t just submit your file. We position it.

We know how to present your income (especially if you’re self-employed) in the best possible light.

We understand which lenders are more flexible about specific risks.

We highlight your strengths, mitigate your weaknesses, and match you with the right product.

We structure the mortgage request so it aligns with a lender’s risk appetite — which can mean a better rate.

Going directly to a lender is like walking into a courtroom without a lawyer. You might be innocent, but good luck arguing your case.

Conclusion: One Word — Risk

The next time you see different mortgage rates floating around, remember this: it all comes down to risk.

Lenders aren’t being inconsistent or unfair. They’re evaluating each borrower based on how likely they are to pay the mortgage — and how costly it will be if they don’t.

The lower your risk, the better your rate.

And if your situation is even slightly outside the cookie-cutter norm, working with a mortgage professional can make all the difference. We help craft your application in a way that reduces the perceived risk, so you don’t leave thousands of dollars on the table over the life of your mortgage.

Don’t Go It Alone

Whether you’re buying, refinancing, or just looking for options, I’d love to help you explore your options and present your profile in the best possible light.

👉 Book a call with me today and let’s figure out how to get you the best deal for your unique situation.