In the complex world of home financing, one common concern among borrowers is the impact of credit inquiries on their credit scores. It's not unusual for borrowers to hesitate about a mortgage credit check, fearing it might lower their overall credit scores. However, it's essential to understand that these checks are a routine part of the mortgage application process and should not cause undue worry.

We’ve heard things like:

“Can’t you just use my free Borrowell report?”

“I don’t want anyone to pull my credit; it will hurt my score!”

Often, borrowers simply want an assessment of their borrowing capacity. While it's possible to evaluate files without accessing their official credit history, doing so is not recommended. Without a complete history and a proper credit report obtained through our system, our advice and opinions on borrowing power come with disclaimers. This is necessary to account for any outstanding balances, loans, or late payments that clients may have forgotten or not disclosed. Additionally, there can be errors in credit reports that need to be addressed.

Understanding Credit Inquiries in Mortgage Applications

As mortgage professionals, we aim to clarify and reassure you about the impact of credit inquiries. Let's discuss why you shouldn't excessively worry about a mortgage credit inquiry.

Here’s the reality:

Minimal Impact: A single credit inquiry typically has a small effect on your credit score, potentially lowering it by just 5 to 8 points.

Credit Score Buffer: Most diligent credit users have a score buffer that compensates for the minor deductions caused by inquiries.

Purpose of Building Credit: Maintaining a good credit history is crucial for significant decisions like buying or refinancing a home.

Lenders Look at Credit Score Ranges: Lenders evaluate mortgage applications using score bands, such as below 600, 600 to 625, 625 to 650, 650 to 680, and 680+.

Avoiding a credit check could hinder your ability to get pre-approved for a mortgage. It's crucial to let your mortgage broker proceed with the necessary checks to ensure you're on the right track to securing your mortgage.

Real-World Case Studies on Credit Inquiries

Case Study 1: The High Achievers with Credit Concerns

Client Story: Edwina & Lionel

Combined Household Income: $187,600

Current Home Value: $750,000

New Home Value: $960,000

Client Goal: Selling their townhome to purchase their forever home

Edwina and Lionel, living in a townhome in Pickering, approached us for a mortgage pre-qualification. Despite their excitement about moving to their forever home, Edwina hesitated to allow a credit check, fearing it might negatively impact her credit score. After reassurance, they agreed to proceed with the inquiry.

Outcome: Edwina had a pristine credit score of 900, the pinnacle of credit health. With such high scores, securing the pre-approval they wanted was straightforward.

Case Study 2: Multiple Inquiries, Minimal Impact

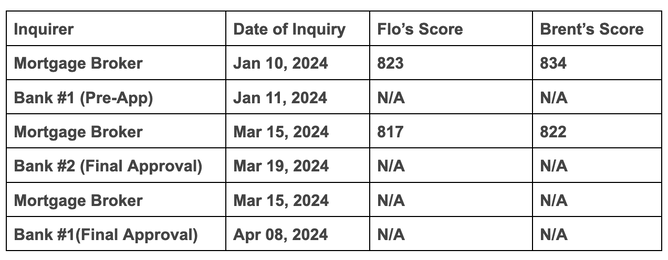

Client Story: Flo & Brent

Combined Household Income: $275,000

Current Home Value: N/A – first-time homebuyers in Canada

New Home Value: $998,000

Client Goal: Purchasing their first home

Flo and Brent, a couple in their late thirties who recently moved to Canada, were ready to buy their first home. Referred by a past client, they were relaxed about the credit scoring process. We had to request credit reports multiple times throughout their mortgage journey, involving negotiations with two different lenders.

Outcome: Despite multiple inquiries, the impact on their credit scores was minimal. Flo's score fluctuated slightly but returned to its original state, while Brent's score dipped modestly but remained well above lender requirements.

Here’s how it played out:

Initial score: Flo started with 823, and Brent with 834.

During the process, Flo’s score fluctuated slightly, dropping to 817 before returning to 823, showing her credit score’s resilience. Brent’s score dipped modestly to 822, well above the lender's requirements.

Final score: By the end of the process, both scores remained strong and high, demonstrating that multiple inquiries (in this case, five consecutive inquiries in the span of 4 months), when done within a proper context, do not have a significant detrimental effect.

On Jan 10th, 2024, we obtained the first credit report and submitted it to the lender for pre-approval. Bank #1 also inquired on Jan 11th before the pre-approval.

On March 15th, 2024, Flo and Brent contacted us with an accepted offer. We submitted the application to Bank #2 as they offered a better option than Bank #1. We also had to obtain another credit report before submitting it to Bank #2 as the first report had expired. Bank #2 also made an inquiry before extending the approval.

However, since the initial approval from Bank #2, we were able to negotiate a better rate for Flo and Brent from Bank #1 and re-submitted the application to them. Since we had obtained a credit report within 30 days, we did not obtain a second report even though we were submitting it to 2 separate lenders.

This experience highlights the importance of not stressing over minor details. Multiple inquiries may seem overwhelming, but in the structured process of mortgage applications, they are just a routine part of the process and have less impact than often feared.

Why Mortgage Credit Inquiries Should Not Deter You

Understanding the nuances of credit inquiries can significantly ease concerns when looking for a mortgage. According to Equifax Canada, multiple mortgage-related inquiries within 45 days only impact your report as a single inquiry. TransUnion Canada states that this is true over a 15-day period.

This minimizes the impact on your credit score and underscores the importance of proceeding with necessary credit checks during the mortgage application process. By demystifying the impact of mortgage credit inquiries, we can help you move forward with confidence, knowing your credit health is secure and your home financing is on track.